valuation

Why “basic” valuation concepts still break deals?

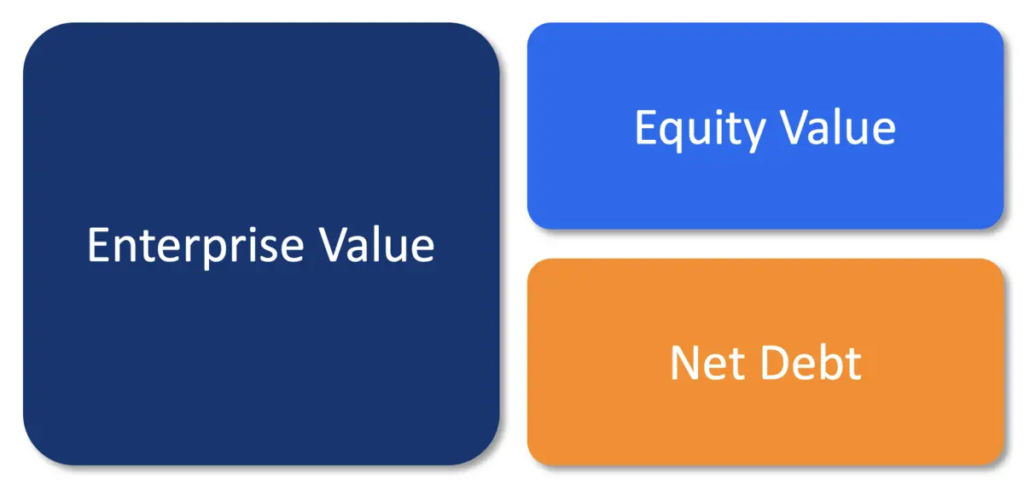

Enterprise Value vs. Equity Value

Enterprise Value (EV) and Equity Value (EqV) are among the first concepts introduced in Corporate Finance 101. While they may appear straightforward—and are often taken for granted by finance professionals—they frequently create confusion among non-finance managers, founders, and shareholders. This is entirely understandable, as finance is not their area of expertise. However, a misalignment in understanding EV and EqV can become a serious deal breaker in M&A transactions. I have seen first-hand how this seemingly basic misunderstanding can derail negotiations and ultimately prevent deals from closing.

Key Takeaways

- EV reflects operating fundamentals, not financing

- EqV is driven by both EV and capital structure

- Cash injections increase EqV, not EV (unless deployed to generate returns)

- Misunderstanding EV vs. EqV can derail negotiations and kill deals

Definitions

Enterprise Value (EV) represents the value of a company’s core operating business, independent of how that business is financed.

Equity Value (EqV) represents the value attributable to shareholders after all debt and other claims are settled.

A simple metaphor helps illustrate the difference:

EV is the value of a house, while EqV is the cash the homeowner walks away with after selling the house and repaying the mortgage.

The relationship between EV and EqV is commonly expressed in the following chart

What Really Changes Enterprise Value

Since EV reflects the value of the core operating business, it only changes when the company’s operating fundamentals change, such as:

- Cash-generation capability

- Growth prospects

- Margins and cost structure

- Capital efficiency (Capex vs. Opex)

- Working capital management

- Risk profile and earnings stability

A critical point worth emphasising is that a cash injection alone does not automatically increase EV. For example, if a company raises new capital but does not deploy it to build a new factory, expand capacity, improve working capital, or otherwise enhance future cash flows, then the company’s future cash-generation potential remains unchanged—and so does its EV

What Really Changes Equity Value

- All factors that impact EV will also affect EqV.

- Capital structure directly impacts EqV

- Debt reduces EqV

- Cash increases EqV

- For instance, a capital injection of $5 million does not change EV, but it increases EqV by $5 million. This is precisely why the concepts of pre-money and post-money valuation exist—both of which refer to Equity Value before and after a new capital injection.

A Real-Deal Story from Practice

During my time in the investment team of a commodity trading company, I evaluated an opportunity to acquire 100% of the shares in an African company.

After a high-level review of historical financial performance and a preliminary valuation, our internal view was:

- Enterprise Value: $60 million

- Net Debt (book value): $40 million

- Equity Value: $20 million

During discussions with the founder of the , we asked about the valuation he had in mind to assess whether our views were aligned.

The founder confidently stated that the Enterprise Value of his company was $45 million.

At first glance, this was clearly inconsistent. If $45 million were truly the EV, then after settling $40 million of net debt, the founder would only receive $5 million in cash proceeds—which was obviously not his expectation.

After several clarification calls, it became clear that the $45 million figure he had in mind was actually Equity Value, not Enterprise Value.

While the transaction ultimately did not proceed due to a valuation gap, this experience strongly reinforced an important lesson:

A clear understanding of Enterprise Value versus Equity Value can materially shape negotiations, expectations, and deal outcomes.